Neo-banks: taking the challenge to a well-established banking sector

The global neo and challenger bank market is expected to reach $578 billion by 2027, at a compounded annual growth rate (CAGR) of about 46.5% from 2019 to 2027. However, these fintech firms are still flying under the radar, triggering the attention and interest of millions of customers worldwide. So, what are Neo-Banks, and what does the future hold for them?

In the wake of the severe 2008 financial crisis, conventional banks, especially in western markets, witnessed a tremendous shock in customer trust, and are now in a constant process of change. This shift in trust has pushed customers to look for other alternatives that can substitute the traditional banks.

Taking advantage of the increased internet and smartphone penetration, a new wave of alternative challenger banks emerged. These are what we call today ‘Neo-banks’. As the term suggests, this new form of banking is disrupting the financial services industry in various ways.

Neo Banks are alternative challenger banks that offer banking services exclusively online. In other words, these fintech firms do not have a physical presence in brick branches. This means that all neo-bank business is conducted through digital means, such as mobile apps and online platforms.

The concept of Neo-bank is new and originated about 5 years ago in the UK, however, they have shown tremendous potential for growth. Some leading banks are already on the right track to scale up. Nubank, the Brazilian digital bank is valued at $10 billion. The company has already raised $820 million throughout its 7 funding rounds and has already attracted 22 million customers in its home country alone. In Europe, the Berlin-based N26 raised $170 million in 2019, at the time it was valued at $3.5 billion.

What is the driving force behind the neo-banking wave?

The world we live in today creates a perfect environment for these firms to thrive. The following trends are driving their growth.

Cashless Payments Trend: Although cash continues to play an important role in payments, emerging innovations are integrating with changing consumer preferences to drive a cashless trend. A prevailing shift toward technology and automation, mobility, and digitization has not ignored the financial services industry.

Blockchain Technology

Blockchain is being used continuously to decrease the overhead costs associated with authenticity validation. In addition, in areas such as financial reporting, compliance, centralized, and business processes, it will help financial institutions reduce expenses by more than 30 percent.

Artificial Intelligence: With about 41 percent of financial companies planning to introduce it in the near future and 20 percent already using its strength, Artificial Intelligence remains a rising FinTech trend that paves the road for more advanced offerings

Customers’ preference for Mobile banking: For 60 percent of banking clients in the United States, mobile connectivity is one of the most significant features. 88 percent of all banking transactions will be via smartphone by 2022.

Neo-Banks customer base keeps widening

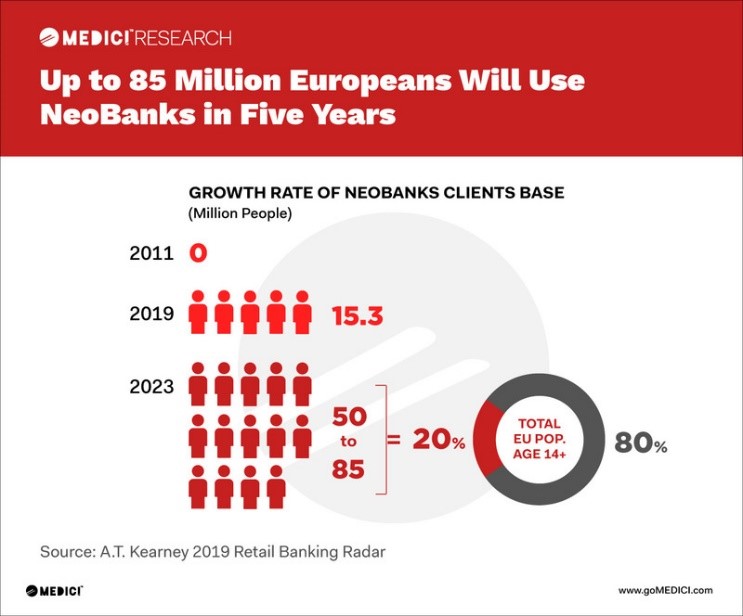

Neo-Banks have been attracting new customers at a mesmerizing rate. In the UK only, they have almost tripled the number of customers in 2019, going from 7.7 million in 2018 to nearly 20 million in 2019 according to Accenture, recording a growth rate of 150% that outpaces that of traditional banks. According to a report by AT Kearney, Neo-Banks in Europe attracted more than 15 million new customers in the period 2011-2019. Their customer base is expected to reach 85 Million by 2023.

Pitchbook, the PE/VC data provider, believes that challenger and neo-banks are major players in the fintech space and have gained millions of customers in recent years. Pitchbook estimates that in 2020, the customer base will reach 60 Million in North America and Europe. They also expect this growth to continue at a CAGR of 25% through 2024, surpassing 145 million customers.

Neo-Banks keep attracting VC/PE capital

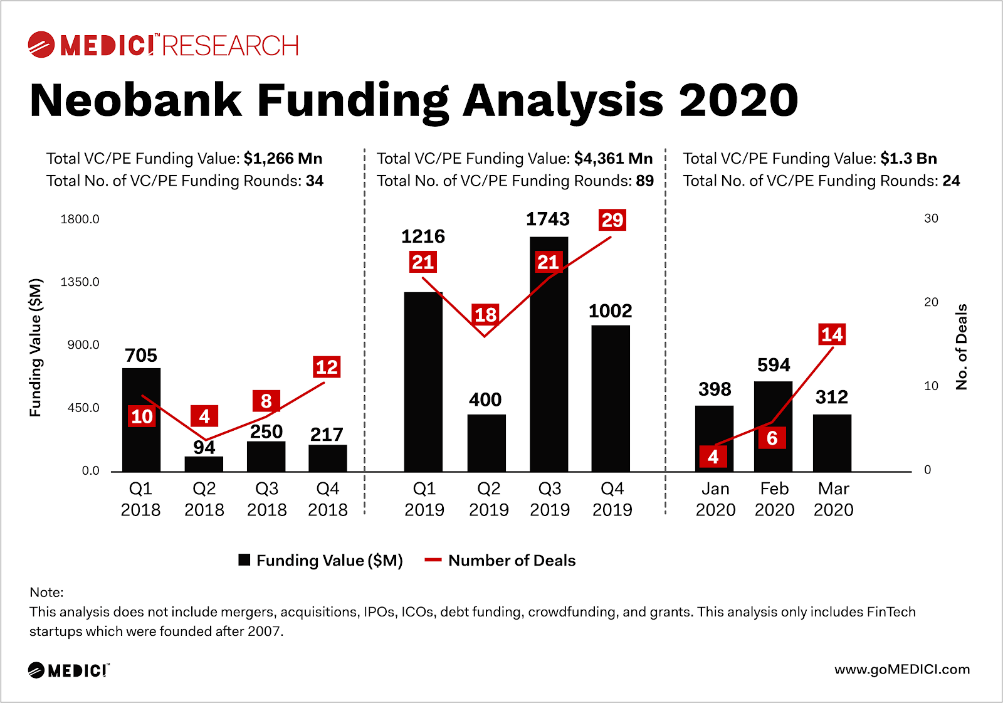

In Q3 2019, Neo banks have recorded an all-time high in Funding. A total of 21 Venture Capital and Private equity financing deals brought these banks around $1.74 billion of capital. In fact, they have raised more than $4 Billion in 2019 only, taking the total capital raised since 2018 to more than $5.5 Billion. As it is the case with most industries in 2020, the capital poured into these companies decreased to just above $1.3 Billion due to the uncertainty brought about by The Coronavirus pandemic. This came as a response to the remarkable business growth of Neo Banks being suddenly halted. Various reasons explain the sudden end to the growth of the market of neo banks. Because of the global lockdown, consumer spending decreased dramatically, as neo banks are mostly used as secondary accounts for unique purposes, they were especially hard hit. In addition, while neo banks are well prepared for a lockdown (being digital and operating remotely), they suffer from conventional banks’ problems. However, Neo banks are far from being excluded from the financial sector despite the uphill struggle they are facing due to the crisis. Even conventional banks have gone down the road of digitalization, following the revolution initiated by fintech. In addition, the COVID-19 pandemic has underlined the need for digital banking. It is a likely scenario that the current crisis will push the financially weaker neo-banks to merge or leave, giving stronger banks their place to drive further growth.

In Q3 2019, Neo banks have recorded an all-time high in Funding. A total of 21 Venture Capital and Private equity financing deals brought these banks around $1.74 billion of capital. In fact, they have raised more than $4 Billion in 2019 only, taking the total capital raised since 2018 to more than $5.5 Billion. As it is the case with most industries in 2020, the capital poured into these companies decreased to just above $1.3 Billion due to the uncertainty brought about by The Coronavirus pandemic. This came as a response to the remarkable business growth of Neo Banks being suddenly halted. Various reasons explain the sudden end to the growth of the market of neo banks. Because of the global lockdown, consumer spending decreased dramatically, as neo banks are mostly used as secondary accounts for unique purposes, they were especially hard hit. In addition, while neo banks are well prepared for a lockdown (being digital and operating remotely), they suffer from conventional banks’ problems. However, Neo banks are far from being excluded from the financial sector despite the uphill struggle they are facing due to the crisis. Even conventional banks have gone down the road of digitalization, following the revolution initiated by fintech. In addition, the COVID-19 pandemic has underlined the need for digital banking. It is a likely scenario that the current crisis will push the financially weaker neo-banks to merge or leave, giving stronger banks their place to drive further growth.

Challenges facing Neo-Banks

It might seem that neo-banks as sailing smoothly towards becoming the new normal. However, they are facing fierce challenges that limit their potential. The following trends are among these challenges.

Differentiators are becoming more and more blurred: Neo-Banks when they first appeared, they were selling themselves as the digital alternative to traditional banks, meaning that they are the best at Mobile and App-based banking. However, traditional banks today offer equally good online banking services on top of their physical presence, eating into what once differentiated neo-banks.

Big well-established banks are offering Neo-Banking alternatives: Traditional banks have been witnessing the speed at which neo-banks have been scaling up lately, so they decided to lunch their own, making the market more crowded and competition even fiercer for the startups.

Their service offerings are limited when compared to their traditional rivals: They do not offer all the services of a traditional bank and are still unable to measure up, not only because of service delivery or regulatory problems but also for lack of capital.

Sacrificing profitability to build a large customer base: In their quest to attract more customers, many banks found themselves sacrificing profitability. Attracting customers with market-leading rates, small to no ATM fees, and above-average interest on savings certainly comes at a cost. This is certainly the case with shared economy giant Lyft that has been losing money since its inception. Lyft operates in a 2-sided marketplace, and it is a difficult place to be in, as the company must ensure that both demand (riders) and supply (drivers) are secure. The methods that Lyft uses to balance its marketplace (discounts, deals, and incentives) can be accounted for in two ways: revenue decreases, or increase in sales and marketing costs, and both of these severely impact the bottom line.

Neo-Banks still have a tremendous potential to explore in the coming years, the rise in mobile and internet penetrations is to create the right infrastructure for their thriving. The increased use and trust in AI and blockchain will take advantage of that infrastructure to drive the growth of neo banks, and protentional lead to a radical shift to the way we do banking. However, pressure from competition and the well-established banking sector represent serious challenges that need to be navigated cautiously.

Othmane Moustahsine – Research Analyst

Sources:

https://thepaypers.com/expert-opinion/the-inevitable-neobank-spring-and-its-drawbacks–780575

https://gomedici.com/neobanks-global-deep-dive

https://gomedici.com/neobanking-2-0-global-deep-dive-2020-report-by-medici

https://www.wpp.com/wpp-iq/from-bricks-to-clicks—the-rise-of-the-neobanks

https://wup.digital/blog/neobank-threat/

https://blog.prototypr.io/10-ways-neobanks-set-themselves-up-for-success-7c1f8f7118c3

https://techcrunch.com/2020/10/02/which-neobanks-will-rise-or-fall/

https://techcrunch.com/2020/03/03/valued-at-10b-nubank-launches-its-nu-credit-card-in-mexico/

https://techcrunch.com/2020/05/05/n26-raises-another-100-million-in-series-d-extension/

https://bfsi.economictimes.indiatimes.com/news/fintech/what-are-neobanks/76128857

https://fincog.nl/blog/18/performance-of-neo-banks-in-times-of-covid-19

https://www.acuitykp.com/blog/can-neobanks-survive-the-covid-19-crisis/

You may also like

Warning: Undefined variable $content in /var/www/sdomains/nexatestwp.com/infomineo.nexatestwp.com/public_html/wp-content/themes/infomineo/single.php on line 235

Warning: Undefined variable $content in /var/www/sdomains/nexatestwp.com/infomineo.nexatestwp.com/public_html/wp-content/themes/infomineo/single.php on line 235

Warning: Undefined variable $content in /var/www/sdomains/nexatestwp.com/infomineo.nexatestwp.com/public_html/wp-content/themes/infomineo/single.php on line 235

Warning: Undefined variable $content in /var/www/sdomains/nexatestwp.com/infomineo.nexatestwp.com/public_html/wp-content/themes/infomineo/single.php on line 235

Warning: Undefined variable $content in /var/www/sdomains/nexatestwp.com/infomineo.nexatestwp.com/public_html/wp-content/themes/infomineo/single.php on line 235

Warning: Undefined variable $content in /var/www/sdomains/nexatestwp.com/infomineo.nexatestwp.com/public_html/wp-content/themes/infomineo/single.php on line 235